Summary

-

The Full Federal Court has dismissed an appeal by

- By reconstructing the reliable hypothetical transaction to be on independent vendor financing terms, including an implied

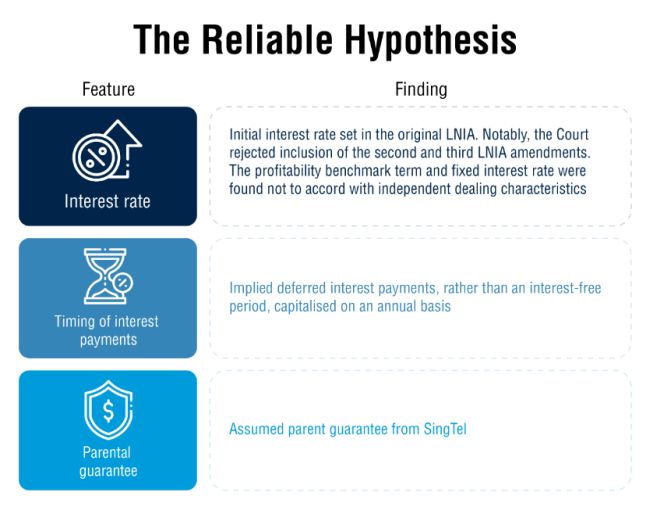

SingTel parent guarantee, the Court concluded STAI received transfer pricing benefits in the income years under review. - The decision provides useful guidance for the application of Subdivision 815-A of the Income Tax Assessment Act 1997 (Cth) (ITAA 1997) and Division 13 of the Income Tax Assessment Act 1936 (Cth) in complex related party arrangements, which although now no longer applicable, should remain relevant in construing Subdivision 815-B of the ITAA 1997. It highlights the importance of considering both commercial substance and the timing effects of a transaction.

- With transfer pricing adjustments expected to trend upward globally, the implications of this case will be keenly followed. Revenue office activity continues to impact the ability of global groups to claim related party deductions.

- The third amendment introduced a fixed rate of 13.5275 percent for the balance of the term of the LNIA.

In a judgment confirming the ATO's approach, the Full Federal Court found STAI had failed to discharge its onus to prove that the assessments were excessive. Led byJustice Wigney , the Court considered issues around: - The amendments of the LNIA diverging from expected independent dealing characteristics

- STAI's expert evidence assessing the "effective credit spread"

Introduction

Under the LNIA, STAI was able to defer payment of accrued interest until the

-

The second amendment forgave any accrued obligation to pay interest and retrospectively ensured that there could be no liability for interest (and therefore no withholding tax) until a profitability benchmark was met. It then added a further interest premium of 4.552 percent to equate to the overall interest expected to be paid over the term for the LNIA if the amendment had not been made.

-

Formulating the appropriate reliable hypothetical scenario for transfer pricing analysis

Issues

Timing of Assessing Non-Arm's Length Conditions

The Court rejected arguments of the taxpayer suggesting that the timing effects of the LNIA should be disregarded. In this regard, STAI sought to demonstrate that the total interest in fact paid by STAI over the entire 10-year term was less than the interest that might have been expected to be paid if an arm's length rate had been agreed upon at the start of the arrangement, and that the assessment of whether there was a non-arm's length dealing could be made at the end of the arrangement with the benefit of hindsight.

In this regard, the Court considered that the statutory context required the Court to consider whether a transfer pricing benefit arose in a particular income year, rather than over the life of an arrangement.

Reliable hypothesis

To apply the relevant tax provisions, the Court had to determine an appropriate basis for comparison to the actual arrangements.

Subdivision 815-A and Division 13 require identifying a hypothetical scenario reflecting independent commercial dealing in similar circumstances. This is called the "reliable hypothesis."

The Court examined factors like the nature of the transaction, characteristics of the parties and evidence from experts.

The Court did not find any errors with the primary judge's characterisation of the reliable hypothesis. In this regard, the Court agreed with the primary judge that the taxpayer's expert evidence regarding interest rates based on a

Implications of

This case provides further guidance (following

Of particular relevance in this case was the fact that the commercial substance of the funding was a vendor financing arrangement, which then impacted the relevance of the taxpayer's expert evidence, which largely relied on comparables in the debt capital market.

The case highlights that taxpayers carry the legal burden of proof and must prepare evidence based on the appropriate hypothetical transaction, rather than rely on theoretical arguments. Further, care should be taken when relying on expert evidence to formulate the reliable hypothesis as this is a legal concept.

Overall, the decision confirms tax authorities' ability to challenge related party arrangements and the high threshold for taxpayers to prove that their international related party dealings do not diverge from independent market conditions between third parties.

Originally published by

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

Alvarez & Marsal

URL: www.alvarezandmarsal.com

© Mondaq Ltd, 2024 - Tel. +44 (0)20 8544 8300 - http://www.mondaq.com, source